A group of energy and climate economists have proposed that a European energy agency be set up to guide the continent’s transition to net-zero carbon by 2050. EneregyEcoLab supports this initiative, which has been signed by Simone Tagliapietra, Georg Zachmann, Anna Creti, Ottmar Edenhofer, Natalia Fabra, Jean-Michel Glachant, Pedro Linares, Andreas Löschel, Joanna Maćkowiak-Pandera, and László Szabó.

As energy and climate economists, we propose that a European energy agency be set up to inform and guide the continent’s transition to net-zero carbon by 2050. Because the energy transition will affect so many operations and interests, an independent public agency is needed to take responsibility for what information should be collected and how it is processed and presented. Stakeholders should be able to suggest improvements to help the agency to steer public planning and private investment. This agency would impartially address questions that are key to formulating energy policy to achieve the transition. Examples include how much industry pays for electricity, the rate at which wind and solar energy are taking over, and which transmission lines are the most congested. The answers are currently unclear, and confused by difficulties in accessing some public statistics and by the fact that updated data are available only commercially. Such a European energy agency could mirror the European Environment Agency and its mandate to deliver knowledge and data to support Europe’s environmental and climate goals. Alternatively, the task could be undertaken by a dedicated branch of the European Union’s statistical office, Eurostat.

The ITRE Committee organises on April 24 a public hearing on the reform of the Electricity Market Design that was proposed by the Commission on 14 March. The proposals aim to accelerate renewable generation and the phase-out of fossil gas, make consumer bills less dependent on volatile fossil fuel prices, better protect consumers from future price spikes and potential market manipulation, and make the EU’s industry clean and more competitive.

The participating experts are:

Konrad Purchała, Managing Director for System Management in PSE

Natalia Fabra, Professor of Economics at Universidad Carlos III de Madrid

Georg Zachmann, Senior Fellow at BruegelProf. Jorge Vasconcelos, Chairman of NEWES

Jaume Loffredo, Senior Energy Policy Officer & Energy Team Leader of BEUC

Members will have an opportunity to exchange views and raise questions with affected stakeholders and experts in the field.

David Andrés-Cerezo wrote this post on uc3nomics Blog, based on research by David Andrés-Cerezo and Natalia Fabra.

Renewable energy sources, such as solar and wind, are becoming increasingly popular to reduce our dependence on fossil fuels. However, these sources are also highly volatile, as their output fluctuates significantly across time and weather conditions: a solar farm cannot generate electricity after the sun sets, and a windmill does not run on calm days. Grid reliability requires that supply always meets demand, but the volatility of renewable energies makes it challenging. For this reason, energy systems worldwide seek solutions to shift supply from periods with abundant renewable energy to those when it is relatively scarce. This is where energy storage technologies come in. These technologies, including batteries, pumped hydro, and compressed air, are a remedy to counteract the variability of renewable energy sources. Moreover, their investment costs have sharply declined, making storage a potentially attractive option for promoting a quick and cost-effective energy transition.

Policy options and regulatory debate

How can renewable energies and storage technologies be encouraged? Is it enough to rely on market incentives, or are other support measures needed? The dramatic decline in the cost of renewable energy investments has promoted a rapid deployment of these technologies. In turn, the volatility of renewable energies will likely enlarge price arbitrage opportunities for firms looking to invest in storage. Finally, the availability of grid-scale storage will boost the value of renewable assets by reducing curtailment in periods when renewable production is large relative to demand. So, is that it?

This logic suggests that renewable energy and storage are complementary technologies, which reduces the need for further support. Still, regulators worldwide are implementing various policies to encourage investments in renewables and storage. For instance, the California Public Utility Commission has implemented a mandate requiring utilities to procure energy storage. Similarly, several European countries, such as Spain, are mandating battery investment as an eligibility requirement for renewable energy subsidies. Beyond the standard goal of correcting environmental externalities, these policy interventions may be motivated by coordination failures that prevent a quick transition to carbon-free power markets. But, are these policies equally effective at every stage of the energy transition? Should they be tailored to the characteristics of each market, such as their solar potential? How do policies to support one technology affect investment incentives for the other?

Modeling electricity markets with energy storage

In a recent article with Natalia Fabra, we seek to answer these questions by modeling investment and operation decisions in wholesale electricity markets. We then quantify the theoretical predictions with simulations of the Spanish electricity market under two scenarios with low and high renewables penetration and different levels of storage capacity.

In our theoretical model, competitive storage and generation firms first decide whether to enter the market and then choose how much to produce and store/release in each hour of each day. Storage operators benefit from arbitraging price differences over time: they buy (charge their batteries) when prices are low and sell (discharge their batteries) when prices are high. The availability of renewable energy affects their profitability as renewables generation might depress prices when the storage facilities charge (in this case, the profitability of storage goes up) or when they discharge (its profitability goes down). Likewise, storage affects the profitability of renewables positively or negatively depending on whether storage operators charge their batteries (which increases prices) or discharge them (which reduces prices) when more renewables are available.

How do we know whether renewables make energy storage operators better or worse off, and vice-versa? Our model predicts that the correlation between renewable availability and market prices is key to explaining their relationship. A negative (positive) correlation means that renewables tend to be available when prices are low (high), which is when storage charges (discharges), thus pushing up (down) the prices at which renewables sell their output, increasing (decreasing) their profitability. Similarly, if this correlation is negative (positive), deploying renewable capacity depresses prices when storage charges (discharges), thus increasing (decreasing) the profitability of storage.

When should we then expect this key correlation to be positive or negative? Electricity prices depend on consumption patterns and solar and wind availability patterns, which vary across markets. Hence, the sign of the correlation between prices and renewables is an empirical question. For this reason, we explore the interaction between renewables and storage in a given context: the Spanish electricity market.

Simulating the Spanish wholesale electricity market

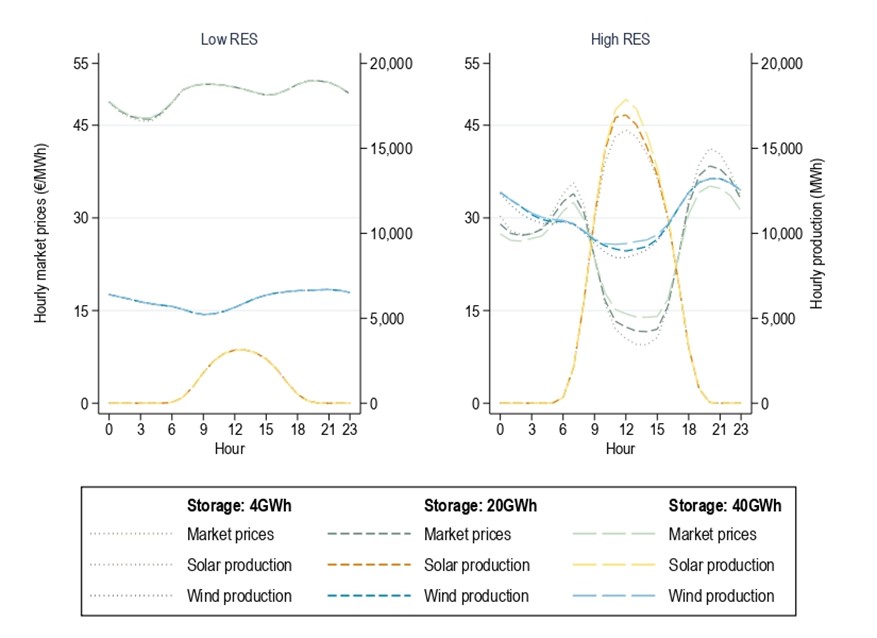

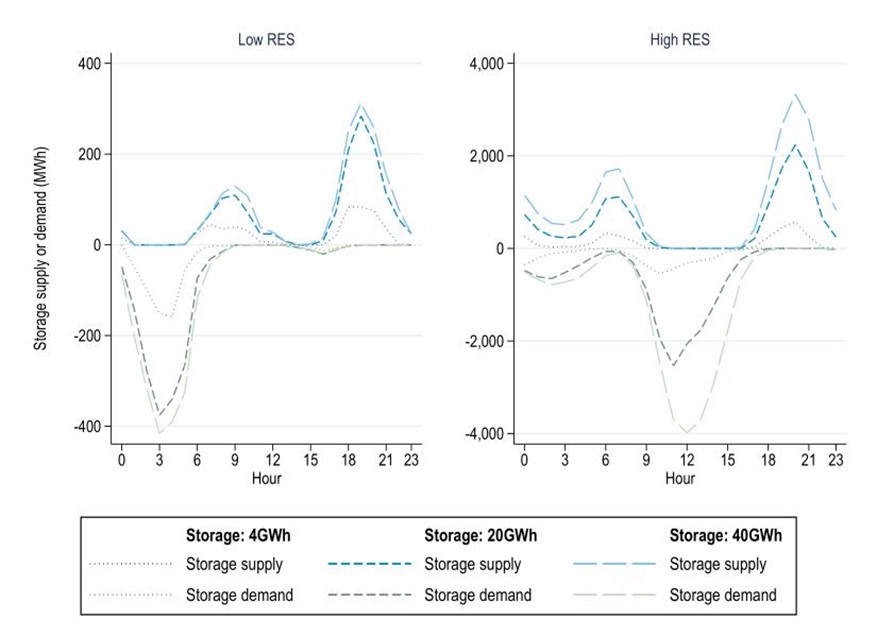

We consider two scenarios: the Spanish electricity market as of 2019, when renewable penetration was relatively low (8.7 GW of solar and 25.6 GW of wind), and the market as it is expected by 2030, when solar and wind capacities are planned to reach 38.4 GW and 48.5 GW, respectively. For each scenario, we consider various levels of storage capacity from 4 GWh to 40 GWh. Figure 1 shows wind and solar production and electricity prices over an average day in 2019 (left panel) and 2030 (right panel). Figure 2 displays (average) hourly storage and release decisions in these two scenarios.

Figure 1: Prices and renewable generation over the day

Figure 2: Charging and discharging decisions over the day

Let us focus on solar production. Figure 1 shows that solar production is concentrated in the intermediate hours of the day. This implies that solar is positively correlated with prices when there are few solar farms (left panel), as solar peaks at noon when consumers’ demand is high. When solar production becomes abundant (right panel), the correlation between prices and solar production becomes strongly negative, as solar generation depresses market prices when available. As a result of this price impact, storage firms shift from charging during nighttime when solar penetration is low (left panel) to charging in the midday hours when solar generation is abundant (right panel).

What does this behavior imply for the profitability of solar plants and storage firms in the Spanish electricity market? At the early stages of the renewable deployment (left panel), entry by an additional solar farm has a negligible impact on storage profits, as the price at which storage charges during the night remains unchanged and solar production does not affect the prices at which storage firms sell their output. Similarly, adding storage capacity has no price impacts at times of solar availability. Hence, the profitability of solar and storage investments remains independent despite the positive correlation between prices and renewables.

However, a big expansion in solar capacity has two effects: it enlarges price differences across the day and makes the correlation between prices and solar production turn negative. As a result, battery utilization increases, and storage profits climb sharply. Similarly, increasing storage capacity from 4 GWh to 40 GWh substantially increases prices in midday hours when storage firms are filling their batteries. Since this coincides with the periods in which solar farms produce energy, their profits go up. This is further compounded by storage allowing more efficient use of solar assets since it reduces energy spills in periods of abundant solar production.

Policy implications

In sum, whether renewables and storage complement or substitute each other might vary from one market to another and differ across time. Policies to promote these technologies should evolve accordingly. In the early stages of solar capacity adoption, prices are typically positively correlated with solar production. Since solar generation is not abundant, it has no price impacts, and the profitability of storage remains independent of how much solar capacity there is. At later stages of the Energy Transition, solar generation depresses prices, turning the correlation between solar generation and prices negative. This implies that increasing storage makes solar firms better off, and increasing solar capacity makes storage firms better off, i.e., they become complements once the correlation is reversed.

Therefore, our findings suggest that a big initial push for renewable investment is necessary to trigger the complementarity between renewable energy and storage. Once the negative correlation kicks in, policies aimed at promoting one technology would come with the additional benefit of promoting the other, shifting the market to a more decarbonized long-run equilibrium.

But this does not set the question once and for all! Future electricity markets may have very different demand and supply patterns from those of today. Therefore, policy design should pay close attention to the specific characteristics of each market at different stages of the energy transition and evolve with it.

Further Reading:

Andrés-Cerezo, and D. Fabra, N. (2023) “Storage and Renewable Energy: Complements or Substitutes?”, Working paper.

About the authors:

David Andrés-Cerezo is Visiting Professor Carlos III University and EnergyEcoLab. He is interested in Energy and Environmental Economics, and Political Economy.

Natalia Fabra is an industrial economist working in the field of Energy and Environmental Economics. She is Professor of Economics at Carlos III University.

Last April 17, Mateus Souza wrote this post on uc3nomics Blog, based on research with Peter Christensen, Paul Francisco, Erica Myers, and Hansen Shao.

Improving the energy efficiency of buildings is often viewed as one of the most promising strategies for climate policy. Retrofit and renovation programs have great potential to abate carbon emissions by lowering households’ energy consumption, which also translates into lower energy bills. These programs can also improve air quality within homes (Tonn, Rose, and Hawkins, 2018) and may even help create jobs (ORNL, 2014). Given all these potential benefits, renovation projects are taking a central role in economic stimulus packets for decarbonization, and for recovering from the recent energy and COVID-19 crises. For example, through the EU’s Recovery and Resilience Facility (EC, 2022), Spain intends to “(support) the green transition through investments of over €7.8 billion in the energy efficiency of public and private buildings.” Similarly, the U.S. Inflation Reduction Act (White House, 2023) projects investments of “$9 billion for states and Tribes for consumer home energy rebate programs, enabling communities to make homes more energy efficient, upgrade to electric appliances, and cut energy costs.”

However, economic evaluations have found that the energy savings from these programs often do not meet expectations. In some cases, the average savings may be as low as 30% of the expected savings (Fowlie, Greenstone, and Wolfram, 2018). This substantially lowers the cost-effectiveness of these programs and puts into question their role in climate policy. Mateus Souza and co-authors dig into this issue with two recent articles. The first helps to identify economic and behavioral explanations of why a “performance wedge” exists between the projected versus the realized energy savings of efficiency programs (Christensen et al., 2021). The second asks whether it is possible to use machine learning tools to improve projections of energy savings, with the objective of better targeting funds to homes that are more likely to benefit from the programs (Christensen et al., 2022).

Decomposing the wedge

To better understand the “performance wedge” in energy savings, we studied the Illinois Home Weatherization Assistance Program (IHWAP). The program provides fully subsidized improvements to the heating, ventilation, and air conditioning (HVAC) systems of low-income family homes in the state of Illinois. We analyzed detailed program information, including data on housing structure, demographics, and energy consumption for more than 9,800 homes. Using a novel machine learning-based approach (Souza, 2019), we investigate the importance of three channels that may explain the wedge: 1) systematic bias in engineering measurement and modeling of savings, 2) work quality during installation of the upgrades (workmanship), and 3) the rebound effect (savings may be offset in case households systematically increase their thermostats once the system becomes more energy efficient).

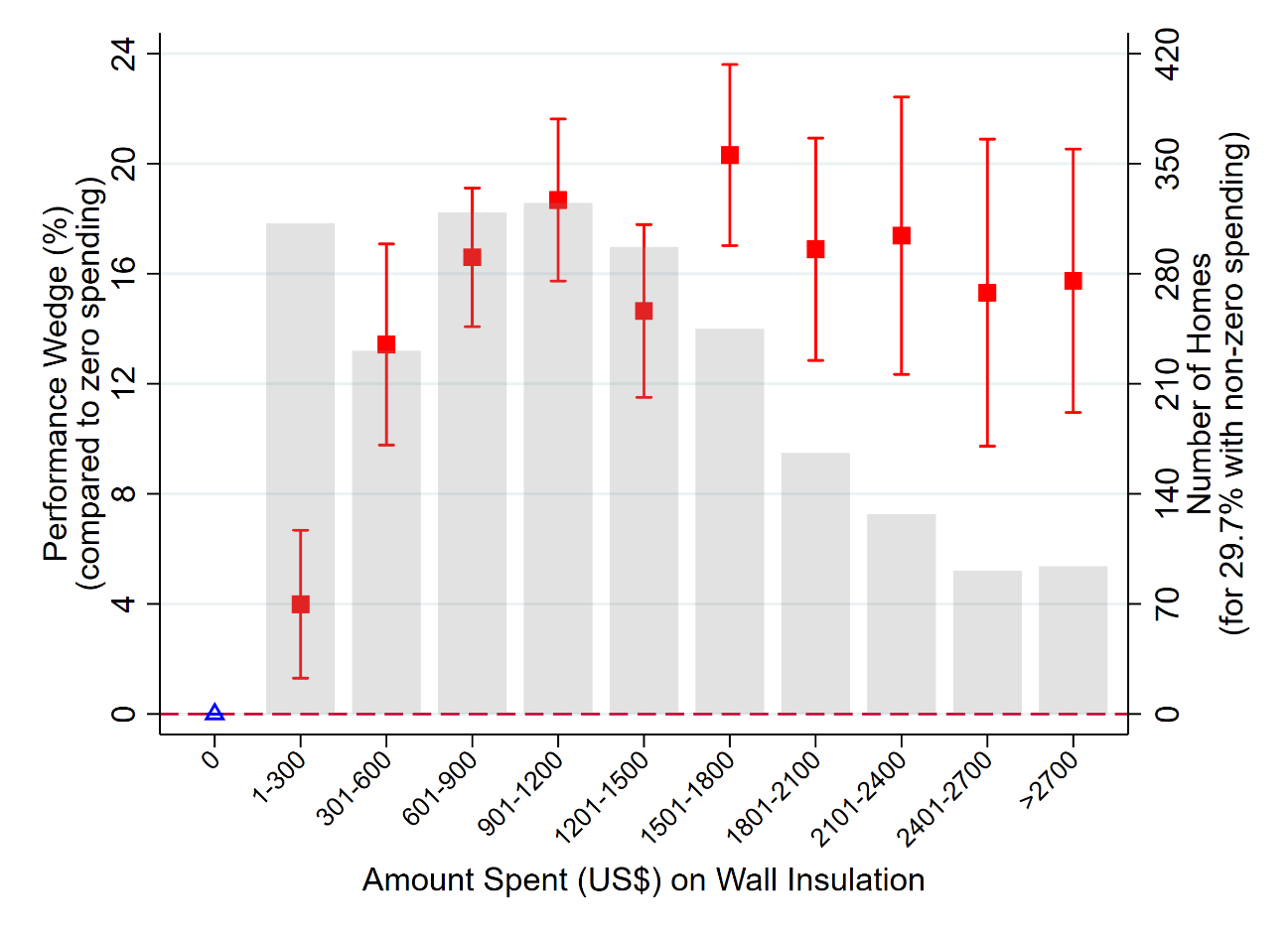

Results suggest that bias in model projections is one of the primary contributors to the wedge. Up to 41% of the wedge can be explained by discrepancies between projected and realized savings in five major retrofit categories: air sealing, furnace replacement, wall insulation, attic insulation, and windows. Results are particularly striking for wall insulation, as shown in Figure 1. The red squares are point estimates of how the performance wedge increases depending on expenditures in that measure, compared to homes that received zero wall insulation spending. The whiskers represent 95% confidence intervals. The figure shows, for example, that the wedge is approximately 20 percentage points higher for homes with wall insulation expenditures between $1,501 and $1,800.

Figure 1: Increased Performance Wedge by Spending on Wall Insulation

Heterogeneity in workmanship is also an important factor in explaining the wedge. Results suggest that the wedge could be reduced by up to 43% if all workers performed at top levels. This implies that there exist potential gains from changing worker incentives, investing in contractor training, etc. On the other hand, only a modest portion of the wedge may be explained by behavioral factors such as the rebound effect. Using data on the realized relationship between outdoor air temperature and energy consumption, we find that households modestly increased their thermostats after weatherization, accounting for only up to 6% of the wedge.

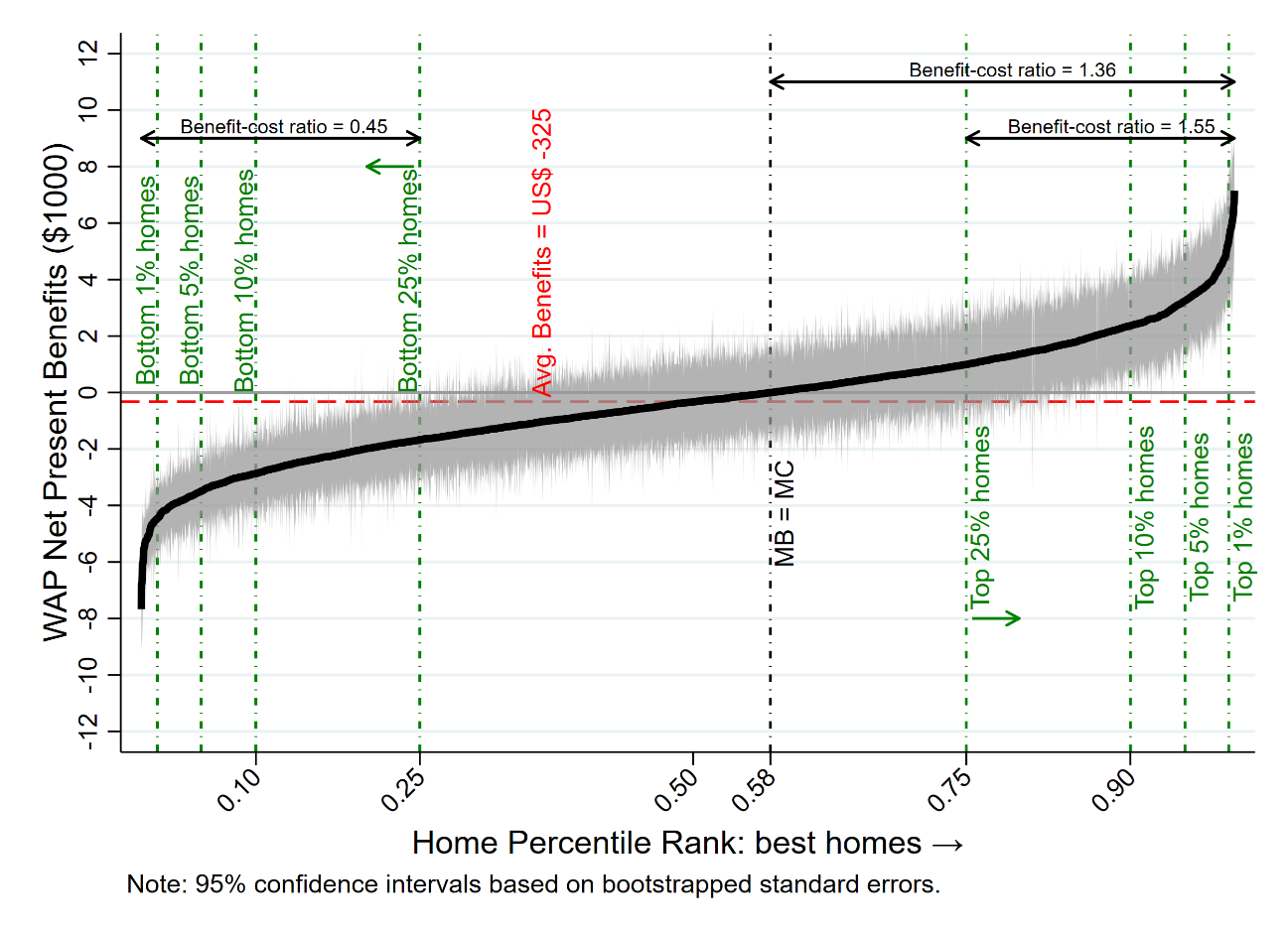

We also analyze the program’s cost-effectiveness by comparing the energy and carbon abatement benefits versus the costs of the retrofits. We find that, on average, each home the program serves is associated with net benefits of -$325. Although average net benefits are close to zero, disaggregated estimates reveal substantial heterogeneity, such that approximately 42% of homes generate positive net benefits, as shown in Figure 2. Therefore, certain types of projects are highly cost-effective, suggesting a potential role for targeting in this context.

Figure 2: Net Present Benefits of Retrofitted Homes

Potential gains from targeting

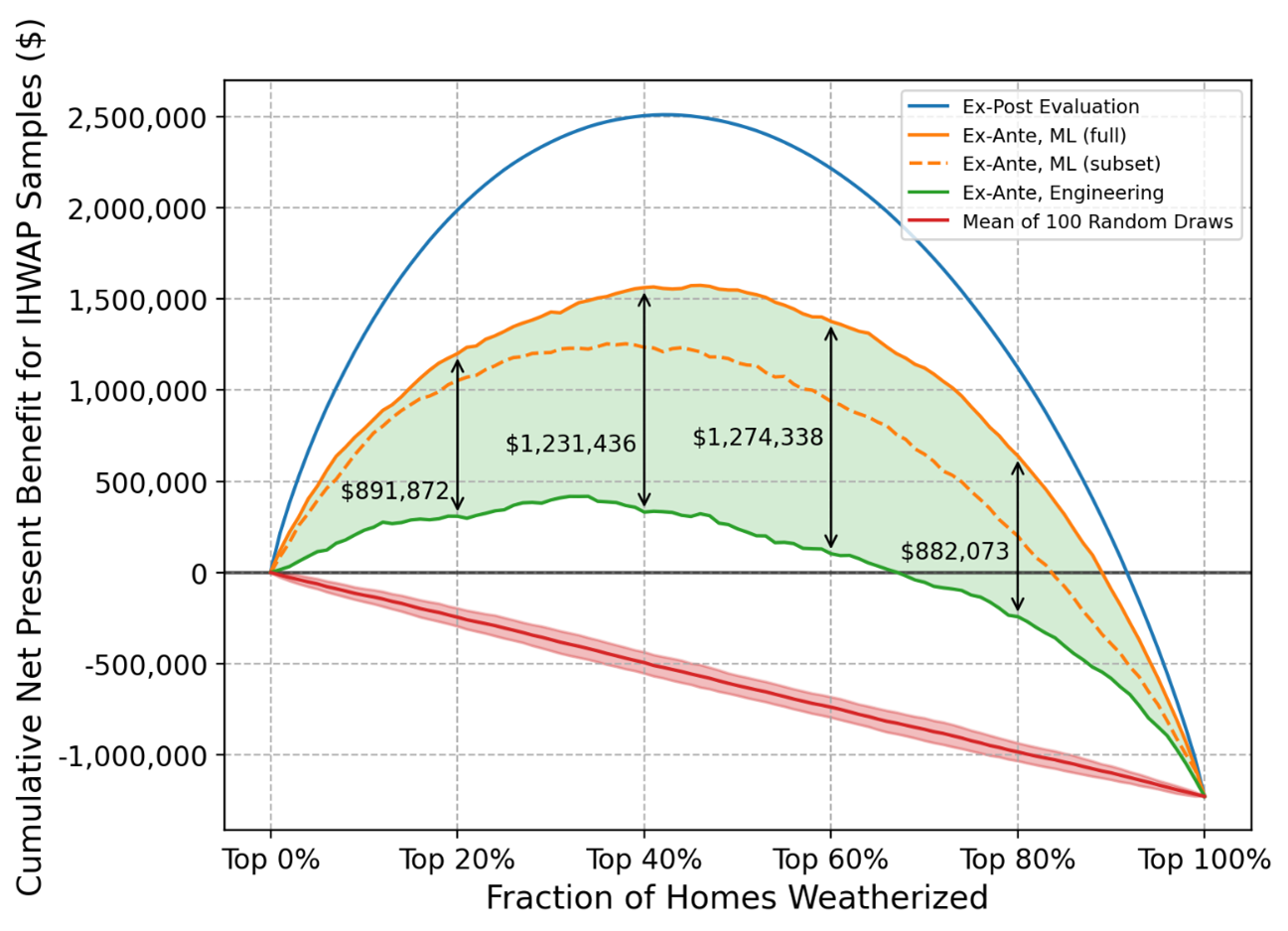

Within this context of substantial heterogeneity in net benefits, a natural follow-up question is whether it is possible to identify the high-return projects before they are actually implemented. We conducted another analysis with data from the same program but now using information available only before the homes were retrofitted. The idea is to mimic the role of a program implementer who is trying to predict the magnitude of net benefits prior to performing the retrofits. To maximize the total predicted net benefits from the program, the implementer would then choose to treat only homes with positive expected returns. This consists of an ex-ante prediction/targeting exercise, which differs substantially from an ex-post evaluation performed with information available many months after the renovations.

As a first step, we show that it is possible to accurately predict home-specific energy savings from the program by using machine learning techniques. In fact, we find that our predictions are accurate even when using a subset of publicly available variables (such as the size and the age of the home, the number of rooms, and the presence of an attic). We then rank homes from highest to lowest net present benefits and calculate the cumulative monetary benefits from retrofitting homes in that order. These results are presented in Figure 3. We compare our machine learning rankings (in orange) to an engineering ranking (in green) that currently guides funding allocation decisions within the program. These are also compared to a ranking with perfect foresight (in blue). Results show that the machine learning strategy outperforms the engineering model and could drastically improve program cost-effectiveness. Within this sample, targeting high-return interventions based on machine learning predictions can dramatically increase net benefits from $0.93 to $1.23 per dollar invested.

Figure 3: Potential Gains from Targeting

Conclusions

Thanks to recent advances in information and data technologies, retrofit programs can readily incorporate machine learning-based strategies to help select among candidate projects. Energy efficiency programs are often sponsored by utilities that have recently developed the data infrastructure to store, query, and serve household billing data. Integrating predictions from machine learning models into those infrastructures would be straightforward. Although these models may be computationally demanding, they only need occasional updates. Once the results are obtained, they can be fed into the backend of existing software that already help with funding allocation decisions.

The importance of considering and implementing these types of tools continues to grow as energy efficiency remains central to climate policy discussions. Optimal allocation of these funds may be crucial to achieve ambitious climate goals. Future work within this context has yet to explore, for example, the distributional implications of targeting investments based solely on energy or climate-related benefits. Analyses of the health and potential job creation impacts of these programs also seem mostly missing from the economic literature.

Further Reading:

Peter Christensen, Paul Francisco, Erica Myers, and Mateus Souza (2021). “Decomposing the Wedge between Projected and Realized Returns in Energy Efficiency Programs.” The Review of Economics and Statistics (Forthcoming); https://doi.org/10.1162/rest_a_01087

Peter Christensen, Paul Francisco, Erica Myers, Hansen Shao, and Mateus Souza (2022). “Energy Efficiency Can Deliver for Climate Policy: Evidence from Machine Learning-Based Targeting.” NBER Working Paper 30467; https://www.nber.org/papers/w30467

Mateus Souza (2019). “Predictive Counterfactuals for Treatment Effect Heterogeneity in Event Studies with Staggered Adoption.” SSRN Working Paper 3484635; EEL Discussion Paper 107; https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3484635

About the authors:

Mateus Souza is a Postdoctoral Researcher at EnergyEcoLab, Department of Economics, Universidad Carlos III de Madrid.

Hansen Shao completed his PhD in Economics in 2021 at the University of Illinois at Urbana-Champaign, and is currently an economic consultant based in China.

Fowlie, Meredith, Michael Greenstone, and Catherine Wolfram (2018). “Do Energy Efficiency Investments Deliver? Evidence from the Weatherization Assistance Program”. The Quarterly Journal of Economics 133, 1597-1644; https://academic.oup.com/qje/article/133/3/1597/4828342

Oak Ridge National Laboratory (2014). “Weatherization Works – Summary of Findings from the Retrospective Evaluation of the U.S. Department of Energy’s Weatherization Assistance Program”. ORNL Technical Report 2014/338; https://nascsp.org/wp-content/uploads/2017/09/ORNL_TM-2014_338.pdf